GUK Magnetics Market Update – July 2026

Date

7 June 2026

Category

Welcome to the GUK Magnetics July Market Update. This update provides an overview of key developments, helping you stay informed and prepared for whatever the market brings.

Make sure to subscribe to our monthly newsletter to receive the latest update in your inbox each month.

July has seen the continuation of the traditional summer shipping peak season, with export activity across China remaining steady as manufacturers continue to support increased third-quarter demand. Production activity remains stable across key manufacturing regions, while forward planning and booking activity remain elevated as businesses continue to manage longer supply chain lead times and evolving compliance requirements.

Trade & Supply Chain Update

Raw Materials & Critical Minerals: Demand for strategic minerals and rare earth materials remains stable, with manufacturers continuing to monitor supply availability closely. Geopolitical considerations, export controls, and regulatory requirements continue to influence procurement decisions and supply chain planning.

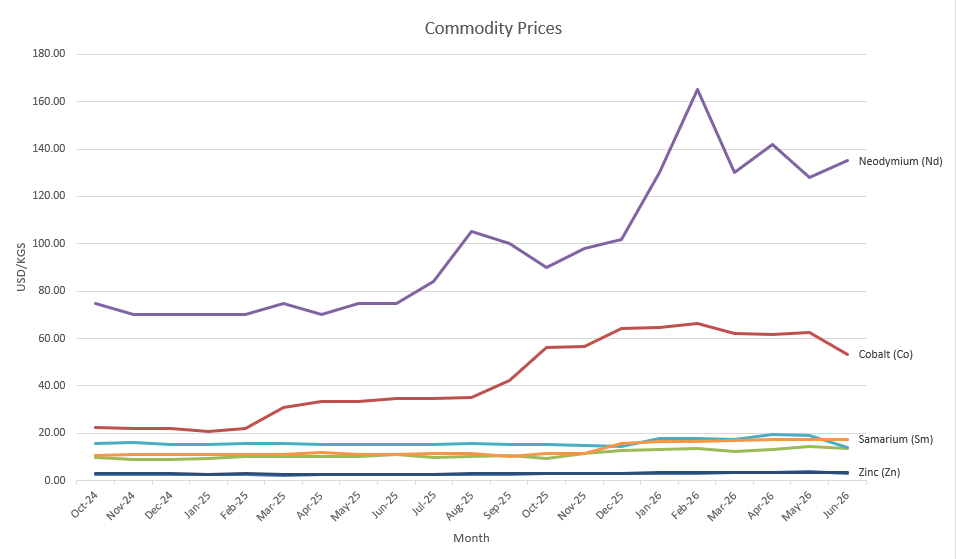

Rare Earth Pricing: Neodymium magnet pricing remains firm, supported by continued demand from electric vehicle, renewable energy, automation, and advanced manufacturing sectors. Market conditions remain relatively stable, although raw material availability and supply-side pressures continue to influence pricing levels.

Compliance & Export Controls: Export compliance requirements remain a key consideration for China-origin shipments, particularly for strategic materials and advanced manufacturing components. Continued regulatory scrutiny and licence requirements may result in extended approval timelines for certain products. Early engagement, accurate documentation, and proactive licence submissions remain essential to minimise potential shipment delays.

China’s Restrictions on Rare Earth Metal Exports: Impacted Products & Export Licence Process

Exchange Rate

Worst GBP to USD exchange rate in June 2026: 1.3165

Best GBP to USD exchange rate in June 2026: 1.3465

Average GBP to USD exchange rate in June 2026: 1.3316

Airport Operations

Air freight demand has remained steady through July as businesses continue to utilise air services to manage urgent requirements and compensate for longer ocean transit times.

Demand & Pricing: Demand remains healthy across key industrial and manufacturing sectors. Air freight rates remain above historical seasonal averages, although pricing conditions have remained relatively stable compared with previous months.

Capacity & Handling: Air freight capacity remains consistent across the major China–UK corridors. Passenger belly capacity continues to recover gradually, providing additional support to the market, although premium services remain in demand for time-critical shipments. UK gateway handling performance, including London Heathrow (LHR), remains generally reliable, with occasional delays possible during periods of increased cargo volumes.

Market Outlook: Air freight markets are expected to remain balanced through the remainder of the summer period. While significant capacity shortages are not currently anticipated, demand for priority and expedited services is expected to remain strong as businesses continue to manage extended ocean freight lead times.

Port Operations

Ocean freight markets have remained firm throughout July, with seasonal demand growth continuing to place pressure on available capacity.

Routing & Transit Times: The Cape of Good Hope routing remains the standard operating pattern for many Asia–Europe services, continuing to add approximately 10–14 days to traditional transit schedules. Schedule reliability has remained relatively stable; however, extended sailing durations and occasional congestion at European gateway ports continue to affect arrival predictability on some UK-bound services.

Capacity & Equipment: Vessel capacity remains available across the main China–UK trade lanes, although utilisation levels have increased as peak season demand continues. Equipment availability remains generally stable across major Chinese export regions.

Rates: Freight rates have remained elevated through July, supported by seasonal demand, longer vessel rotations due to Cape routing, and continued carrier capacity management. Peak season surcharges remain in place on selected services, with spot rates continuing to experience upward pressure where capacity is more constrained.

Commodity Rates

As the summer peak season progresses, supply chains are expected to remain influenced by longer ocean transit times, firm freight costs, and ongoing regulatory requirements. Businesses maintaining proactive forecasting, early order placement, and appropriate inventory planning will be best positioned to manage requirements through the remainder of 2026 and into 2027.

While overall market conditions remain stable, continued flexibility and forward planning remain essential to maintaining reliable China–UK supply chain performance.

The GUK Magnetics team remains committed to supporting your manufacturing and logistics strategy. If you would like to review your current orders, discuss upcoming requirements, or plan your forward supply chain needs, please get in touch — we are here to support your business at every stage.